You did the hard part. You built the traffic, optimized your ad placements, signed up for the affiliate networks, and watched your AdSense and Mediavine deposits grow month over month. Your blog is finally generating real, meaningful income. And then one day you try to rent a new apartment, refinance your mortgage, or finance a car, and you hit a wall you never saw coming: nobody will accept your income because you cannot prove it.

This is the documentation gap that almost every successful online publisher eventually runs into, and it is more common than the monetization community likes to admit. The Federal Reserve has reported that self-employed and gig-based workers are significantly more likely to be denied credit or discouraged from applying than traditionally employed workers with comparable incomes. The skills that make you good at monetizing a website have nothing to do with the paperwork the financial world expects, and that mismatch can cost you an apartment, a favorable mortgage rate, or a business loan you genuinely qualify for.

This guide breaks down exactly why online income is so hard to document, what banks and landlords actually want to see, and the step-by-step system you can build to turn your scattered monetization revenue into income that the financial world recognizes and accepts.

Why Online Income is So Hard to Prove

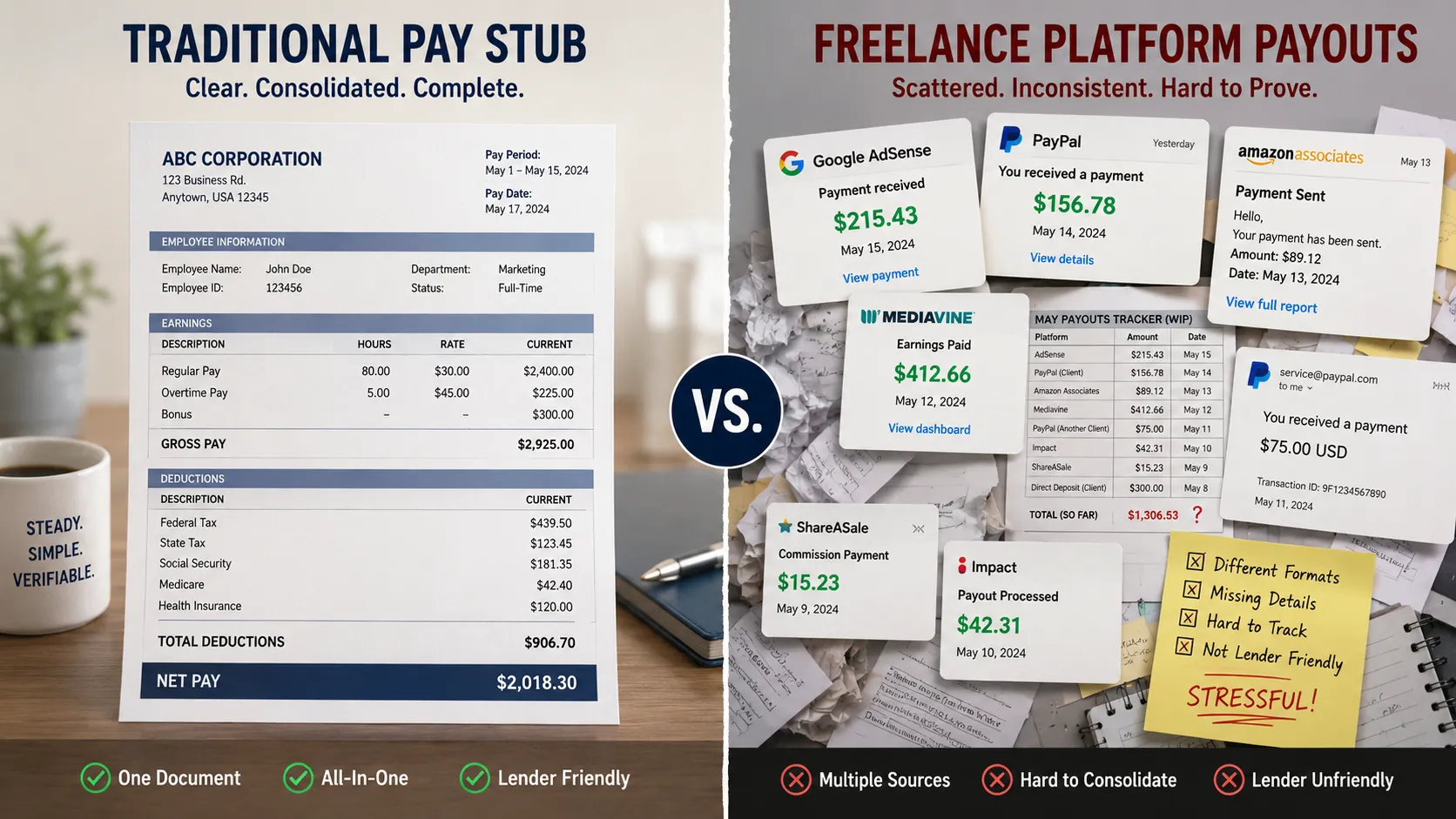

When someone works a traditional job, their employer generates a pay stub every pay period and a W-2 at year-end. Banks, landlords, and lenders recognize these documents instantly. They are the universal language of income verification, and the entire financial system is built around evaluating them.

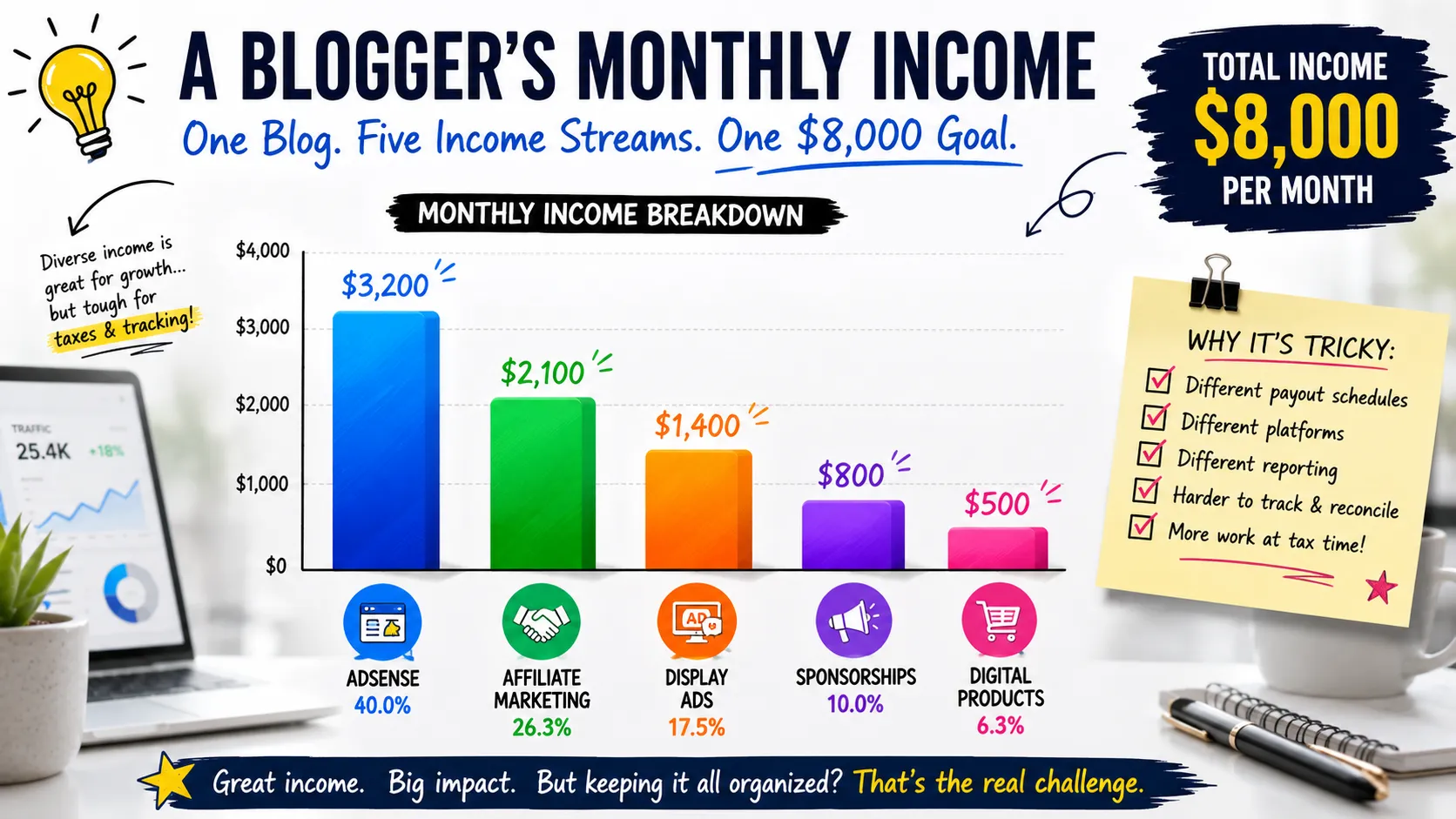

Your blog income speaks a completely different language. It arrives as a scattered mix of deposits, each on its own schedule and in its own amount:

- An AdSense payment around the 21st of each month, but only once you cross the $100 payout threshold.

- Affiliate commissions from Amazon Associates, typically paid roughly 60 days after the month they were earned.

- Display ad revenue from Mediavine or Raptive, paid on net-65 terms.

- Sponsorship payments via PayPal or direct deposit, on whatever schedule each brand negotiates.

- Digital product sales through Gumroad or Teachable, paid out on rolling cycles.

Every platform pays differently, none of them withhold taxes, and none of them produce a unified document showing your total income. To a loan officer trained to read W-2s and pay stubs, this looks like financial chaos, even when it adds up to a consistent six-figure annual income. The underwriter is not trying to be difficult. They simply have no standardized document to evaluate, so they default to caution.

The result is a frustrating paradox that thousands of full-time creators experience: publishers who earn well above the income needed to qualify for an apartment or loan get denied anyway, purely because their income does not arrive in the format institutions are built to assess.

What the Financial World Actually Wants to See

Before you can solve the problem, it helps to understand what lenders and landlords are really trying to determine. At the core, they are answering a single question: is this income reliable, sufficient, and likely to continue? Every document they request is designed to answer that question.

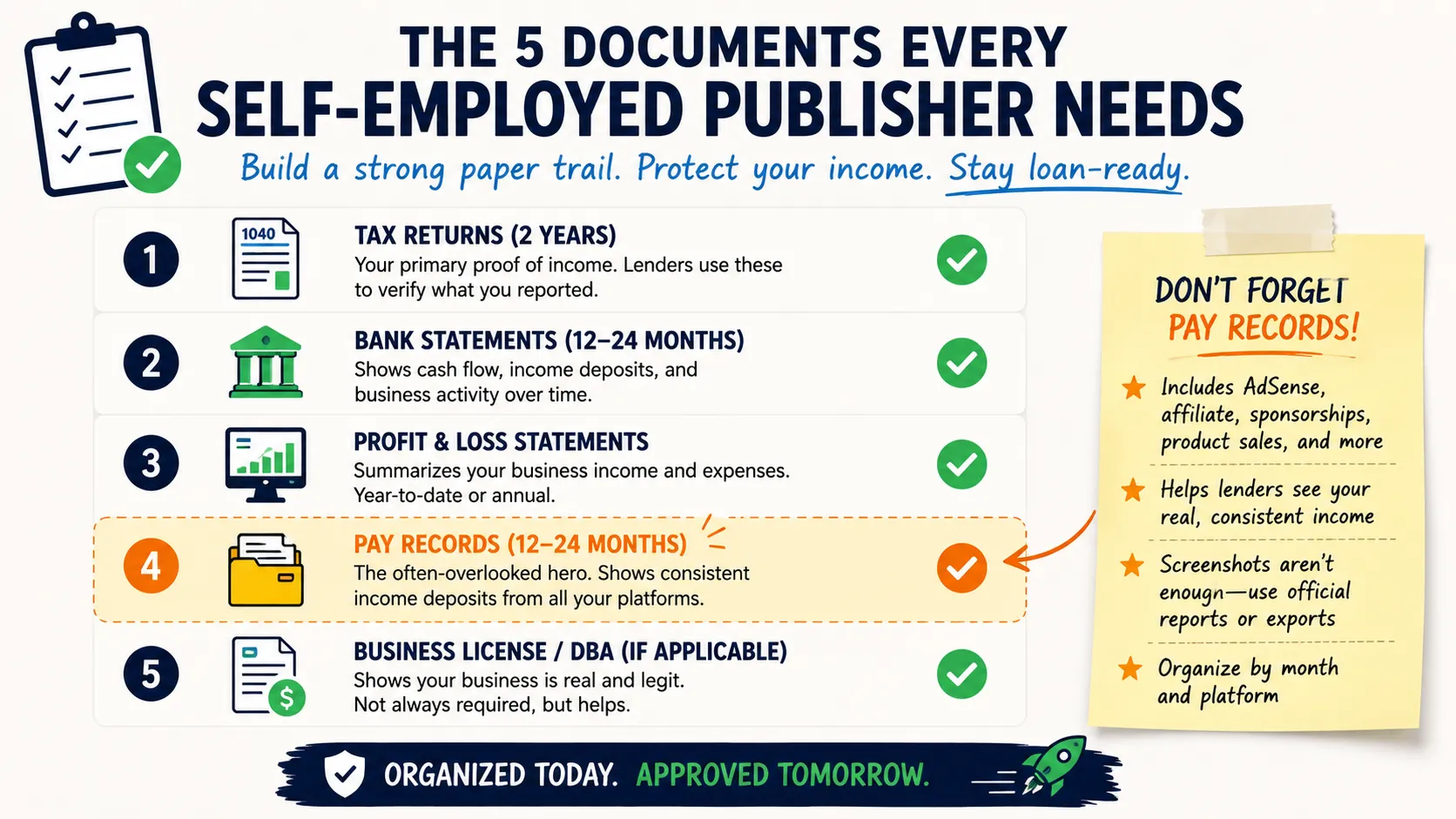

For a self-employed publisher, satisfying that question usually requires assembling several documents that, together, tell a consistent story:

- Tax returns from the past two years, which establish a track record and are the gold standard for self-employed income verification

- Bank statements from the past three to six months, which demonstrate consistent deposits

- 1099 forms from the networks and platforms that paid you more than the reporting threshold

- A profit and loss statement summarizing your publishing business income and expenses

- Pay records documenting the regular salary you draw from the business

That last item is the one most bloggers completely overlook, and it is frequently the difference between an application that sails through underwriting and one that gets buried in repeated requests for additional documentation. Tax returns show last year. Bank statements show raw deposits without context. But a consistent set of pay records shows something more powerful: that you run a real operation and pay yourself a predictable, documented income.

Step One: Separate Your Business and Personal Finances

The single most important shift is to stop treating your blog income as money that simply appears in your personal checking account, and start treating it as revenue that flows through a real business. This is the foundation everything else is built on.

Open a dedicated business bank account and route every stream of monetization income through it: AdSense, affiliate payouts, ad network deposits, sponsorships, product sales, all of it. This accomplishes three things at once. It creates a clean, reviewable transaction history. It establishes your operation as a legitimate business in the eyes of lenders. And it makes your bookkeeping and tax preparation dramatically simpler, because your business activity is no longer tangled up with your grocery runs and Netflix subscriptions.

If you have been operating your blog through your personal account using your Social Security number, this is also the moment to apply for an Employer Identification Number (EIN) from the IRS. It is free, takes about five minutes online, and it protects your personal information while reinforcing the separation between you and your business.

Step Two: Pay Yourself on a Consistent Schedule

Once your income flows through a dedicated business account, the next step is to pay yourself a consistent amount on a regular schedule. Pick a day (monthly is the most common choice for online publishers because it aligns with most platform payout cycles), and transfer a set amount from your business account to your personal account.

That transfer is now your self-employed paycheck. It does not need to equal your full monthly revenue. In fact, it should not, because you need to reserve money for taxes and reinvestment. The goal is consistency: a steady, predictable amount that mirrors how a traditional salary works. If your blog income fluctuates month to month, which almost every blog income does, paying yourself a smoothed, consistent figure actually strengthens your documentation, because lenders prize stability over raw size.

A practical guideline many creators follow is to reserve 25 to 30 percent of revenue for federal, state, and self-employment taxes, set aside a portion for reinvestment and business expenses, and pay themselves the remainder as a consistent salary.

Step Three: Document Each Payment Professionally

Once you are paying yourself consistently, you need to document each payment in a format the financial world recognizes. This is where most publishers either give up or rely on a messy spreadsheet that no underwriter will take seriously.

Using a pay stubs generator lets you produce clean, professional documentation for each pay period in minutes. You enter your gross pay, your estimated tax withholdings, and the pay period dates, and the tool generates a standardized pay stub that mirrors what a traditional employer would issue. Done consistently each month, this transforms your scattered AdSense and affiliate deposits into exactly the kind of recognizable income record that landlords and lenders are trained to evaluate.

The key is consistency and accuracy. Each pay stub should correspond to an actual transfer from your business account, and the amounts should reconcile against your bank statements. Six months of regular, verifiable pay records looks like a functioning business with a stable owner salary. A single pay stub generated the night before a rental application looks like exactly what it is, and experienced underwriters can spot the difference immediately.

A Note for Publishers Who Also Work as Contractors

Many bloggers and digital marketers earn income from more than just their owned properties. You might write for clients, manage other people’s ad campaigns, consult on SEO, or ghostwrite newsletters. This contract income is treated differently from your owned-site revenue, and it comes with its own documentation considerations.

If a meaningful share of your earnings comes from contract work, it is worth understanding the complete guide to generating an independent contractor pay stub, which walks through how contractor pay records differ from traditional employee pay stubs, what information they should contain, and how to document project-based income so it holds up for financial applications. Combining clean records from both your owned sites and your contract work gives you the strongest, most complete picture of your total income, which is exactly what a lender wants to see from a self-employed applicant with multiple revenue streams.

Step Four: Keep Everything Organized and Accessible

Documentation only helps you if you can produce it on demand. Build a simple system now so you are not scrambling later:

- Store your monthly pay stubs in a dedicated cloud folder, labeled by date

- Save the 1099s from every platform as they arrive each January

- Keep your business bank statements downloaded and organized by month

- Maintain a running profit and loss statement (updated monthly) that your accounting software can generate automatically

- Retain your filed tax returns and supporting documents for at least three years

This habit takes maybe ten minutes a month once it is set up, and it means that the day you decide to apply for a mortgage or sign a new lease, your entire financial history is ready to hand over in a single organized package.

Build the System Before You Need It

The publishers who struggle with income documentation are almost always the ones who wait until they need it. They decide to buy a house, then scramble to reconstruct two years of financial history from scattered platform dashboards and PayPal exports, and discover too late that the records simply do not exist in a usable form. Underwriters want to see consistency over time, and you cannot manufacture a two-year history overnight.

The publishers who breeze through are the ones who set up their systems early, often a year or more before they actually need them. They opened the business account, started paying themselves on a schedule, generated their pay records each month, and kept their documents organized from the beginning. By the time they applied for financing, they had a clean, consistent, professional financial history ready to go.

The Bottom Line

Monetizing a website is a genuine entrepreneurial achievement, but the financial world does not automatically recognize it as one. Bridging the gap between earning online income and proving it comes down to four things: treat your blog like a business, pay yourself like an employee, document that income in a format institutions accept, and keep everything organized and accessible.

Do that consistently, and the next time a landlord or lender asks you to prove your income, you will hand them professional documentation instead of trying to explain what Mediavine is and how affiliate commissions work. Your monetization skills built the income. The right documentation habits are what let you actually use it in the rest of your life.

Your Next Steps

If you are earning meaningful income from your website, do not wait until you are denied a loan to fix this. Take these actions this week:

- Open a dedicated business bank account and apply for a free EIN from the IRS

- Route all of your monetization income through that account going forward

- Choose a monthly date and amount to pay yourself a consistent owner salary

- Generate a professional pay stub for that payment, and repeat it every month

- Set up a cloud folder to store your pay stubs, 1099s, and bank statements

Start this month, stay consistent, and within half a year you will have built the kind of income documentation that turns your online revenue into real-world financial credibility.